When you buy an S&P 500 fund, you think you're buying 500 companies. You're not. You're making a roughly 40% bet on ten of them.

As of early 2025, the ten largest companies in the index — Apple, Nvidia, Microsoft, Alphabet, Amazon, Meta, Tesla, Broadcom, Berkshire Hathaway, and Walmart — make up close to 40% of its entire value. The other 490 share what's left. Seven of those names, the so-called "Magnificent Seven," drove more than half of the index's total return in 2024.

So when someone tells me their portfolio is "diversified across 500 companies," what they actually own is a large, concentrated position in a handful of U.S. mega-cap technology firms, wearing the costume of broad diversification.

That isn't automatically a mistake. But it is a decision — and most people making it don't know they're making it. This piece is about what that decision really is, the honest case for and against it, and why, for the money you plan to retire on, we do something different.

The mechanism is simple and not sinister: the S&P 500 is market-cap weighted. Each company's slice of the index is set by its size, so as the biggest companies get bigger, they take up more of the index — and more of your outcome. You don't choose this concentration. It accumulates quietly, in the background, every time the largest names outrun the rest. After a multi-year run led by a few enormous technology companies, the result is an index far more top-heavy than its 500-name label suggests.

More concentrated than the dot-com peak.The index is more heavily weighted toward its top ten names today than it was at the height of the dot-com bubble in 2000. The label says "broad market." The math says "big bet on a short list."

I'm going to make the other side's argument as well as its smartest proponents would, because you deserve that — and because the lazy version of this article, the one that pretends indexing is obviously foolish, would insult your intelligence.

The case is strong:

If someone hands you this list and you nod along — good. You should. Any honest argument for global diversification has to survive it. Here's the one I think does.

My objection is not the one you're expecting. I am not predicting that the S&P 500 will underperform. I don't know that, and neither does anyone confidently selling you the opposite. Anyone who tells you they know which region or sector leads the next decade is guessing with conviction.

My objection is about asymmetry — about what happens to you if the concentrated bet goes wrong, weighed against what you give up if it goes right.

If you're globally diversified and the S&P keeps winning, your cost is real but survivable: you trail the headline number, you feel the FOMO, you still compound at a healthy rate and fund your life. If you're concentrated and that handful of companies stalls, your cost is not symmetric — especially in retirement, when you're withdrawing rather than adding. Selling shares of a falling, concentrated portfolio to fund living expenses permanently destroys capital that can't recover when the market does. This is sequence-of-returns risk, and it is the difference between a comfortable thirty-year retirement and outliving your money.

Concentration is exactly what makes that downside fat. And we have watched it happen — more than once:

None of these were predicted in advance. Each looked, beforehand, exactly like a safe bet on the obvious winner. That's the point. The risk you can't see is the one that ends retirements.

This is where the long-run record is actually useful — not as a promise that global beats domestic, but as proof that leadership changes hands and no one rings a bell when it does.

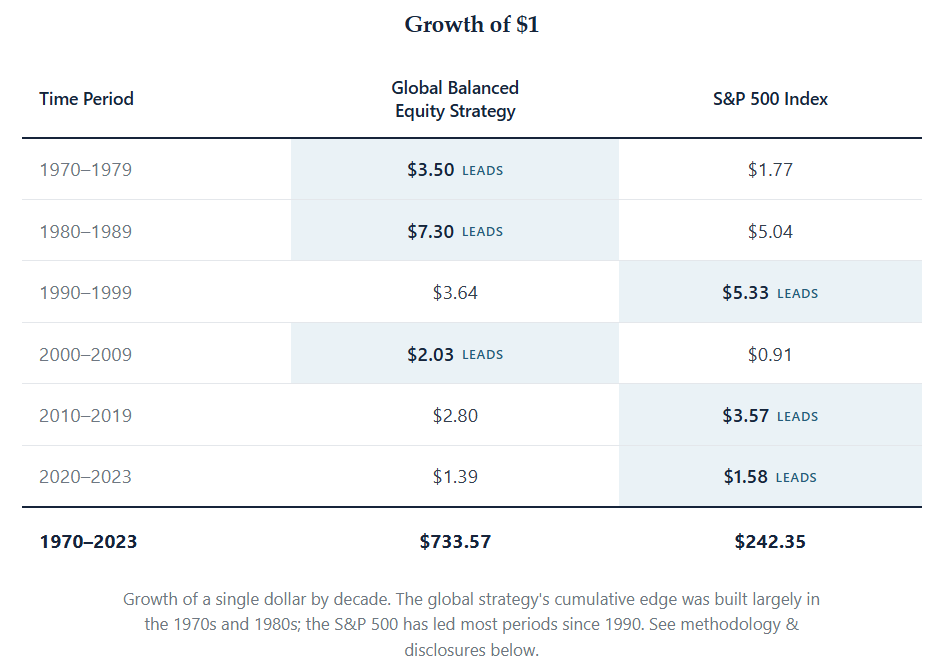

Compare a globally diversified strategy against the S&P 500 decade by decade, going back to 1970. The highlighted cell marks which approach led each period.

Read the table honestly, because it doesn't say what a lazy advisor would claim it says.

It does not say "global always wins." Look closely: the global portfolio's biggest edge was built in the 1970s and 1980s. Since 1990, the S&P 500 has led most decades — including the most recent one, decisively. If you only studied the last fifteen years, you'd conclude concentration is genius.

What the table actually says is more useful and more humbling: leadership rotates, the rotations last a long time, and they are obvious only in the rear-view mirror. Sometimes the U.S. mega-caps lead. Sometimes the rest of the world does. The one thing no investor — not you, not me, not the manager on TV — has reliably done is call the turn in advance.

If you can't predict which slice leads next, the disciplined move isn't to guess. It's to own all of it, and to size each piece so that no single bet can sink the plan.

We build globally diversified portfolios spanning more than 13,000 companies across roughly 50 countries, deliberately tilted toward the factors that decades of evidence associate with higher expected returns, and managed with tax efficiency at every step.

A few things follow from that design, on purpose:

That's the whole philosophy: a portfolio engineered for the resilience of your goals, not the entertainment of your statements.

Because it's genuinely hard — not intellectually, but emotionally.

It's hard to hold positions that lag the headline index for years and feel, every quarter, like you're missing the party. It's hard to ignore financial media built to make you act. It's hard to look diversified next to a neighbor who went all-in on the winners and looks like a genius — right up until they don't.

Discipline isn't complicated. It's just uncomfortable, repeatedly, for a long time. That discomfort is the price of admission, and it's precisely why the strategy keeps working: if it felt easy, everyone would do it, and the edge would disappear.

"Just buy the S&P 500" isn't wrong because it's a bad index. It's risky because it has quietly become a concentrated bet that most of its owners don't realize they've made — more top-heavy today than at the dot-com peak, with the entire downside landing on you, at the moment you can least afford it.

Diversification doesn't mean owning more of what's already winning. It means owning what you can't predict, sized so the unpredictable can't ruin you. The path to lasting wealth isn't chasing last year's leaders. It's committing to a process built to survive every decade — including the ones nobody sees coming.

If you'd like to see what your own plan looks like under this lens, including where you may be more concentrated than you think, that's a conversation we're always glad to have.

[i] The Standard and Poor’s 500 is an unmanaged, capitalization weighted benchmark that tracks broad-based changes in the U.S. stock market. This index of 500 common stocks is comprised of 400 industrial, 20 transportation, 40utility, and 40 financial companies representing major U.S. industry sectors. The index is calculated on a total return basis with dividends reinvested and is not available for direct investment.

[ii] The Uncommon Average: Long-Term Context on Annual Returns | Dimensional

[iii] SPY – Performance – SPDR® S&P 500® ETF Trust | Morningstar

[iv] SPY – Performance – SPDR® S&P 500® ETF Trust | Morningstar

[v] S&P 500 Companies by Weight

[vi] Top 20 S&P 500 Companies by Market Cap (1989–2025) – FinHacker.cz

[vii] Stock Market Gains Flow Mostly To Handful Of Companies | Investor's Business Daily

[viii] A Tale of Two Decades: Lessons for Long-Term Investors | Dimensional